Credit Card Hardship Programs: What Issuers May Offer

Hardship programs vary by issuer, but common options include reduced interest, waived fees, temporary payment reductions, and short-term account relief.

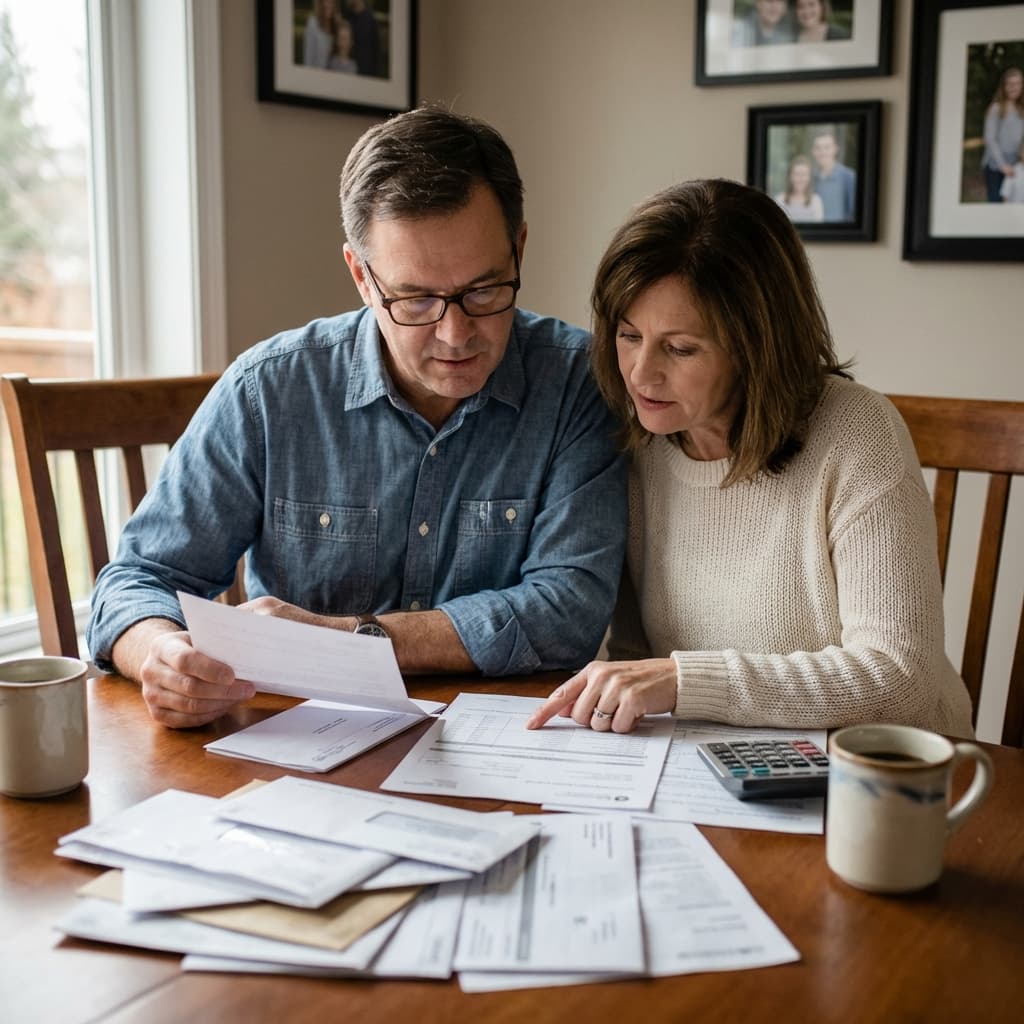

Why people miss this option

Many cardholders assume hardship help only exists after default. In reality, issuers may have internal programs designed to reduce risk before things deteriorate further.

The catch is that you usually have to ask directly and explain the problem clearly.

What an issuer may offer

A lower interest rate, smaller minimum payment, late-fee relief, or a defined hardship plan are all common possibilities. To request one, a short hardship letter makes the ask easier to approve.

Some programs come with restrictions, such as account suspension or a requirement to close the card while you repay.

How to call more effectively

Call before you are far behind if possible. State the hardship, explain what payment is realistic, and ask whether a hardship or customer-assistance program exists.

If the first representative only gives a generic answer, ask whether there is a retention, recovery, or account assistance team. If repayment is no longer realistic at all, compare debt consolidation vs settlement before committing.

This content is for educational purposes only and does not constitute financial advice. Consult a licensed financial professional for advice specific to your situation.

MoneySimple may receive compensation from partners featured on this page. This does not influence our editorial opinions or recommendations.

Debt relief programs may affect your credit score and may involve fees. Results vary. Consider consulting a nonprofit credit counseling agency.

Related articles

More guidance from Debt Relief.

Get smarter about money.

Free weekly tips on credit, debt, taxes, and more.

No spam. Unsubscribe anytime.